In Singapore, HDB flats are not only the homes of the majority of residents but also a key pillar of social stability. According to official data, about 80% of Singaporeans live in public housing developed by the Housing & Development Board (HDB).

So, who is eligible to apply for a Build-To-Order (BTO) flat? And what are the criteria for buying a resale flat?

Today, we’ve compiled the latest comprehensive guide to help you understand everything in one read!

Eligibility & Criteria for BTO Applications

To apply for a BTO flat in Singapore, you must first meet the following basic requirements:

Which Schemes Qualify You for BTO?

1. Public Scheme

You must form a core family unit with one of the following groups:

- Spouse and children

- Parents and siblings

- Unmarried children under legal custody

2. Fiancé/Fiancée Scheme

- Apply together with your fiancé/fiancée

- Must register your marriage and submit the marriage certificate within three months after collecting the keys

3. Orphans Scheme

- Applicant is an orphan, and at least one deceased parent was a Singapore citizen or PR

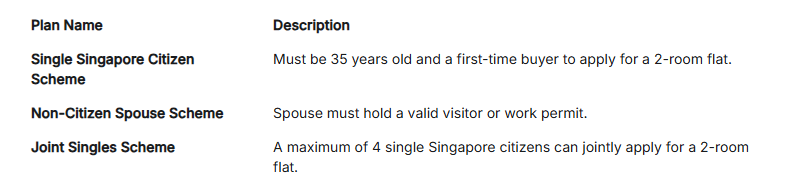

What If You Don’t Qualify for the Above Schemes?

Even if you don’t meet the above schemes, you may still have alternative ways to apply for a BTO flat, depending on your circumstances.

First-Timer vs Second-Timer: What’s the Difference?

First-Timer Applicants

- Have never received any housing subsidy or similar benefit

- If your spouse is a second-timer but you are a first-timer, you will both still be considered first-timers when applying together

Advantages:

- Higher allocation of BTO flats

- Eligible for priority schemes

- More ballot chances (depending on the scheme)

- Additional ballot opportunities if unsuccessful in non-mature estate applications

- May qualify for deferred income assessment and staggered downpayment schemes

Second-Timer Applicants

- Have previously owned an HDB/DBSS/EC flat or received housing grants

Advantages:

- Access to affordable short-lease 2-room Flexi flats

- Eligible for HDB concessionary loans

- May qualify for grants and subsidies

- Certain priority allocations

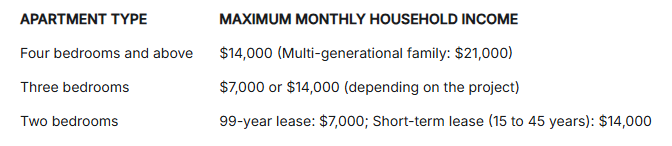

Income Ceiling (Applicable to BTO Applications Only)

The following types of income are included for HDB income assessment:

- Regular allowances (fixed/variable), e.g. meal, transport, laundry, uniform

- Living allowances

- Study allowances

The following types of income are not included:

- Alimony

- Bonuses

- Directors’ fees

- Overtime pay (temporary)

- Interest from savings accounts

- National Service allowances

- Rental income

- Overseas scholarship allowances

- Overseas living allowances

- Pension

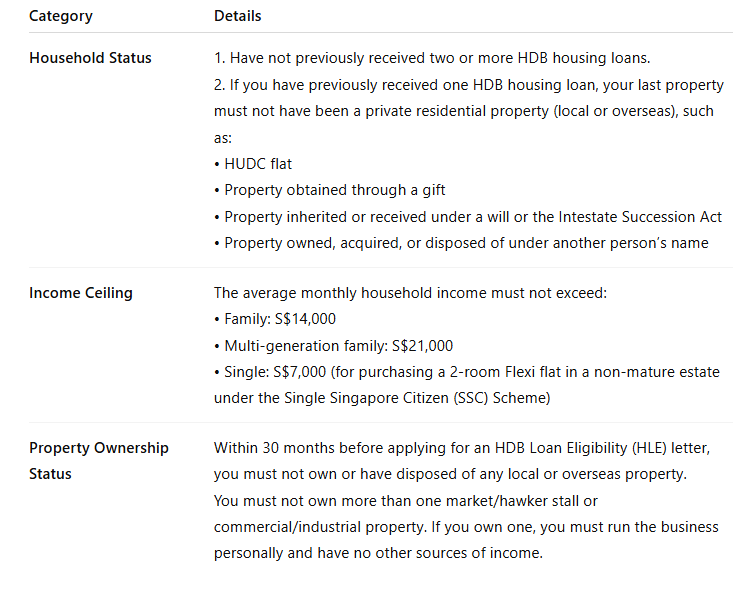

Loan Options: HDB Loan vs Bank Loan

HDB Loan Eligibility:

(Conditions apply based on income, citizenship, and property ownership.)

Bank Loan:

- You may choose any bank

- Loan-to-Value (LTV) ratio is up to 75% of the flat’s value

- A 25% downpayment is required, of which at least 5% must be in cash; the remaining 20% can be paid using CPF Ordinary Account (OA) savings

- Loan amount and interest rate depend on credit assessment

Singapore’s public housing policies are complex but fair — designed to ensure that HDB flats are prioritized for residents who need them most.

Whether you are a first-time buyer or planning to upgrade your home, understanding the eligibility conditions and schemes will help you plan your housing journey with greater confidence.

This article summarizes current HDB policy information for reference only. For updates, please refer to official sources.